Document control:

Document control information

Policy Name: Counter Fraud Bribery and Corruption Policy

Policy Number: C006

Version: 1.0

Status: Final – Approved

Author / lead: Assistant Governance Manager

Responsible Executive Director: Executive Director of Finance & Commercial

Responsible Committee: Audit, Risk & Compliance Committee

Date approved by Responsible Committee: 24 March 2026

Date ratified by the ICB Board/Effective Date: 1 April 2026

Next review date: April 2028

Target audience: EICB staff (including temporary/ bank/agency staff)

– Contractors engaged by the EICB

– Staff from other Essex ICS Partnership organisations working on behalf of the ICB

Stakeholders engaged in development of policy (internal and external):

– Local Counter Fraud Specialist`

– Associate Director of Governance Executive Director of Finance & Commercial

– Audit Risk and Compliance Committee

Impact assessments undertaken: Equality Impact Assessment (see Appendix A)

Version history:

Version: 0.1

Date: 10/02/2026

Author (Name and title): Jane King, Governance Support Manager

Summary of amendments made: Draft EICB Policy

Version: 1.0

Date: 24/03/2026

Author (Name and title): Helen Chasney, Governance Senior Officer

Summary of amendments made: Final – Approved version

Introduction

This is a controlled document. Whilst this document may be printed (please consider if this is necessary), the electronic version posted on the intranet is the controlled copy. Any printed copies of this document are not controlled. As a controlled document, this document should not be saved onto local or network drives but should always be accessed from the website (or requested from the Governance Lead/Team) to ensure the most up-to-date version is used.

All fraud, bribery and corruption (collectively referred to as economic crime) in the NHS is unacceptable and must not be tolerated. It affects the ability of the NHS to improve health outcomes for the population, as resources are wrongfully diverted and cannot be used for their intended purpose. NHS funds and resources must, therefore, be safeguarded against those minded to committing economic crime.

The Essex Integrated Care Board (EICB or ‘the Board’) is absolutely committed to maintaining an honest, open and well-intentioned culture within the organisation. It is, therefore, also absolutely committed to the identification and elimination of fraud, bribery or any other illegal act which occurs either within or against the organisation.

Whilst every effort will be made to prevent fraud and bribery from occurring, where this is not possible, the Board is committed to the rigorous investigation of any such cases and robust controls to ensure where identified it can be eliminated and prevented in the future. Consequently, all cases of suspected fraud, bribery and dishonesty will be considered for investigation. Where appropriate, criminal prosecution and civil court action may be taken to recover money, costs and interest. Employees of the ICB or of third parties acting on behalf of the ICB may also be subject to criminal/civil/disciplinary action and or referral to a professional regulator.

The Board wishes to encourage anyone having reasonable suspicions of fraud and/or bribery to report them. Therefore, it is also the Board’s policy, which will be rigorously enforced, that no individual will suffer in any way as a result of reporting a reasonably held suspicion, provided that they have acted in ‘good faith’ when doing so. For these purposes ‘reasonably held suspicions’ shall mean any suspicions other than those, which are raised maliciously and found to be groundless. The Board is also committed to ensuring employees are treated in line with the Public Interest Disclosure Act 1998 and its Freedom to Speak Up (Whistleblowing) Policy (Ref HR001), which should be consulted by employees who are concerned about making a report.

Purpose / Policy Statement

The overall aim of this policy is to:

- Improve the knowledge and understanding about the risk of fraud, bribery, and corruption within the ICB and that such offences are unacceptable.

- Assist in the promotion of a climate of openness, and a culture and environment where staff feel comfortable to raise concerns sensibly and responsibly.

- Set out the ICB’s responsibilities with the deterrence, prevention, detection, and investigation of fraud, bribery, and corruption.

- Ensure the appropriate sanctions are considered following an investigation, which may include any or all of the following:

- Criminal prosecution.

- Civil proceedings.

- Internal / external disciplinary action, including by professional or regulatory bodies.

The ICB is committed to the elimination of fraud within the ICB, and wider NHS; to the rigorous investigation of any such allegations, and to taking appropriate action against wrong doers, including possible criminal prosecution, as well as undertaking steps to recover assets lost due to fraudulent activity, and ensuring its resources are appropriately protected from fraud, bribery and corruption.

The ICB expects anyone with reasonable suspicions of fraud to report them. The ICB recognises that, whilst cases of theft are usually obvious, there may initially only be a suspicion regarding potential fraud and, therefore, employees should report the matter to the Local Counter Fraud Specialist who will then ensure that processes are followed. Any person who becomes aware of fraud, bribery, or corruption and does not follow this policy could be subject to disciplinary action. Please refer to the ICB’s Disciplinary Policy (Ref HR015).

Scope

This policy applies to all ICB staff (including temporary/ bank/agency staff), contractors engaged by the ICB, staff from other Essex ICS Partnership organisations working on behalf of the ICB and external parties that have a business relationship with the ICB.

The Local Counter Fraud Specialist (LCFS) will investigate any fraud that may cause a loss to the NHS, and this may include internal fraud i.e. committed by an employee, or external including an individual, supplier, or a criminal organisation.

Definitions

Fraud – The Fraud Act 2006 focuses on the dishonest behaviour of the subject and their intent to make a financial gain or cause a financial loss. The gain does not have to succeed if the intent is there.

The key Fraud Act 2006 offences are:

- Fraud by false representation: knowingly making an untrue or misleading statement. The representation may be express or implied and by any means e.g., by words or actions.

- Fraud by failing to disclose: involves not saying something when you have a legal duty to do so e.g., failing to disclose criminal convictions.

- Fraud by abuse of position: abusing a position where there is an expectation to safeguard the financial interests of another person or organisation.

- Making or supplying articles for the use in fraud: e.g., false qualification certificates.

- Obtaining services dishonestly: e.g., falsifying car parking permits to avoid parking charges.

Fraud carries a maximum sentence of 10 years imprisonment.

Property – means any property whether real or personal (including things in action and other intangible property).

Gain – includes a gain by keeping what one has, as well as a gain by getting what one does not have.

Loss – includes a loss by not getting what one might get, as well as a loss by parting with what one has.

NHS Counter Fraud Authority (NHS CFA) – this is the Special Health Authority charged with identifying, investigating, and preventing fraud and other economic crime within the NHS and the wider health group. Focused entirely on counter fraud work, the NHS CFA is independent from other NHS bodies and directly accountable to the Department of Health and Social Care. The NHS CFA has responsibility for all policy and operational matters relating to the prevention, detection, and investigation of fraud, bribery, and corruption in accordance with the NHS CFA guidance ‘tackling crime against the NHS: a strategic approach.’ The NHS CFA’s 2023-2026 Strategy sets out their key priorities for the coming years to protect from fraud, bribery, corruption and details how they will deliver them to reduce fraud affecting the NHS.

Government Functional Standard – A requirement in the NHS Standard Contract is that relevant providers of NHS services must take the necessary action to comply with the Government Functional Standard 013: Counter Fraud (Functional Standard), including having policies, procedures, and processes in place to combat fraud, bribery, and corruption to ensure compliance with the Standards.

NHS funded services are required to provide the NHS CFA with details of their performance against the Functional Standard annually. To this end, the NHS CFA have a suite of requirements tailored to enable NHS organisations to meet the Functional Standard. This includes the requirement that the organisation has a counter fraud, bribery and corruption policy and response plan that follows NHS CFA’s strategic guidance and has been approved by the executive body or senior management team.

Additionally, Service Condition 24 of the NHS Standard Contract enables the commissioner’s nominated LCFS, a person nominated on their behalf, or a person nominated to act on the NHS CFA’s behalf, to review the counter fraud provisions put in place by the provider.

Bribery and Corruption – the Bribery Act 2010 came into force on 1st July 2011. Generally, bribery is defined as giving someone a financial or other advantage to encourage that person to perform their functions or activities improperly or to reward that person for having already done so; or requesting, agreeing to receive, or accepting the advantage offered.

The general offences under the Act are:

- To offer, promise, or give a financial or other advantage to another individual to bring about the improper performance by another person of a relevant function or activity and to reward that improper performance.

- To request, agree to receive or accept a bribe where the individual knows or believes that the acceptance of the advantage offered, promised, or given constitutes the improper performance of a relevant function or activity. This is referred to as passive bribery.

- Promise, offer, or give a financial advantage to a foreign public official or through a third party, where such an advantage is not legitimately due.

- Failure of commercial organisations to prevent bribery on their behalf. Applies to all commercial organisations to prevent bribery on their behalf. Applies to all commercial organisations which have business in the UK. Applies to the commercial organisation itself, as well as to individuals and employees acting on their behalf.

The maximum penalty for bribery is 10-years imprisonment, with an unlimited fine. In addition, the Act introduces a corporate offence of failing to prevent bribery by an organisation not having adequate preventative procedures in place. The ICB may avoid conviction if it can show that it had procedures and protocols in place to prevent bribery. The corporate offences is not a standalone offence but always follows from a bribery and / or corruption offence committed by an individual associated with the company or organisation in question.

Economic Crime and Corporate Transparency Act 2023 (ECCTA) and the Failure to Prevent Fraud Offence

The ECCTA is a UK law designed to tackle economic crime and enhance corporate transparency. The ECCTA aims to increase transparency of corporate entities and introduces legislative changes to facilitate the prosecution of corporations for fraud and economic crime failings.

The ECCTA contains, amongst other things, a new corporate offence of Failure to Prevent Fraud, which came into effect on 1st September 2025, and the transformation of Companies House from a largely passive recipient of information to a much more active gatekeeper.

Under the Failure to Prevent Fraud offence, an organisation may be criminally liable where an employee, agent, subsidiary, or other ‘associated person’, commits a fraud intending to benefit the organisation and the organisation did not have reasonable fraud prevention procedures in place. In certain circumstances, the offence will also apply where the fraud offence is committed with the intention of benefitting a client of the organisation. It does not need to be demonstrated that directors or senior managers ordered or knew about the fraud.

The offence sits alongside existing law; for example, the person who committed the fraud may be prosecuted individually for that fraud, while the organisation may be prosecuted for failing to prevent it.

The offence will make it easier to hold organisations to account for fraud committed by employees, or other associated persons, which may benefit the organisation, or, in certain circumstances, their clients. The offence will also encourage more organisations to implement or improve prevention procedures, driving a major shift in corporate culture to help prevent fraud.

The offence applies to large organisations only and applies across the UK. More information, including what is meant by ‘large organisations’ and the impact on NHS organisations, can be found on the NHS Counter Fraud Authority website.

A senior manager is someone who plays a significant role in either:

- the decision making about how the whole or a substantial part of the organisation’s activities are managed or organised; or

- the actual managing or organising of the whole or substantial part of those activities.

This covers both those in the direct chain of management as well as those in strategic or regulatory compliance roles.

Money Laundering – Money laundering is a process by which the proceeds of crime are converted into assets, which appear to have a legitimate origin, so that they can be retained permanently or recycled into further criminal enterprises.

Legislation defines money laundering as:

‘Concealing, converting, transferring criminal property or removing it from the UK; entering into or becoming concerned in an arrangement which you know, or suspect facilitates the acquisition, retention, use or control of criminal property by or on behalf of another person; and/or acquiring, using or possessing criminal property.’

The Proceeds of Crime Act 2002 applies to all transactions and can include dealings with agents, third parties, property or equipment, cheques, cash or bank transfers. Offences covered by the Proceeds of Crime Act 2002 and the Money Laundering Regulations 2007 may be considered and investigated in accordance with this Policy and the Anti-Crime and Corruption Response Plan.

The ICB could become indirectly involved in this act where the proceeds of any crime, e.g. fraud, are converted by making a payment to the ICB and then seeking immediate repayment.

Theft – theft is defined within the Theft Act 1968 as ‘dishonestly appropriating property belonging to another with the intention of permanently depriving the other of it.’

The Theft Act 1968 also includes robbery, burglary, and abstracting electricity amongst other offences.

Should theft or similar offences be suspected by any person the ICB’s Local Security Management Specialist (LSMS) should be informed to review security measures and recommend referral to the Police if appropriate.

Computer Misuse Act 1990 – The Computer Misuse Act protects personal data held by organisations from unauthorised access and modification.

The Act makes the following illegal:

The Theft Act 1968 also includes robbery, burglary, and abstracting electricity amongst other offences.

- Unauthorised access to computer material. This refers to entering a computer system without permission (hacking).

- Unauthorised access to computer materials with intent to commit a further crime. This refers to entering a computer system to steal data or destroy a device or network (such as planting a virus).

- Unauthorised modification of data. This refers to modifying or deleting data and also covers the introduction of malware or spyware onto a computer (electronic vandalism and theft of information).

- Making, supplying, or obtaining anything which can be used in computer misuse offences.

These four clauses cover a range of offences including hacking, computer fraud, blackmail, and viruses.

Failure to comply with the Computer Misuse Act can lead to fines and, potentially, imprisonment.

Roles and Responsibilities

Integrated Care Board

The ICB Board is accountable and responsible for ensuring that its resources are appropriately protected from fraud, bribery, and corruption. The ICB Board is assured through the work of the Audit Committee.

Audit, Risk and Compliance Committee

This committee is responsible for the detailed oversight and scrutiny of the systems and processes for protecting the ICB from fraud, bribery, and corruption.

The Audit Committee will:

- Require assurance that there are adequate arrangements in place for tackling economic crime.

- Approve the counter fraud, bribery, and corruption work plan.

- Review the outcomes of counter fraud, bribery, and corruption work.

- Review the adequacy and effectiveness of policies and procedures, seeking reports and assurances from Officers as appropriate.

Chief Executive

The Chief Executive is responsible for implementation of and compliance with this Policy. The Chief Executive has overall responsibility for the funds entrusted to the ICB and, as the Accounting Officer, will ensure adequate policies and procedures are in place to protect the ICB from economic crime.

Executive Director of Finance & Commercial

The Executive Director of Finance & Commercial, as a member of the Board, is responsible for overseeing and providing strategic management and support for all work to tackle economic crime within the ICB.

This ensures there is effective leadership and a high level of commitment to the tackling of economic crime within the ICB. Identifying a member of the Board to oversee this work also helps the ICB to focus on its key strategic priorities in the area of economic crime.

All counter fraud, bribery, and corruption services (including for hosted bodies) are provided under arrangements proposed by the Executive Director of Finance & Commercial and approved by the Audit and Assurance Committees, on behalf of the Boards.

The Executive Director of Finance & Commercial, in consultation with the LCFS, will decide whether there is sufficient cause to investigate, and whether the Police and External Audit need to be informed.

The Executive Director of Finance & Commercial or the LCFS will consult and take advice from the Associate Director of People & OD if a member of staff is to be interviewed or disciplined in accordance with the ICB’s Disciplinary Policy. The Executive Director of Finance & Commercial or LCFS will not conduct a separate investigation, but the employee may be subject of a separate investigation by the People and OD Function.

The Executive Director of Finance & Commercial will, depending on the outcome of investigations (whether on an interim / on-going or a concluding basis) and / or the potential significance of suspicions that have been raised, inform the Audit Risk and Compliance Committee Chair of cases, as deemed appropriate and necessary

NHS Counter Fraud Authority

In accordance with its case acceptance criteria, the NHS Counter Fraud Authority (NHS CFA) will investigate cases of fraud that are not investigated by the ICB Counter Fraud Team.

The ICB will provide access to and support for NHS CFA improvement activity and will fully engage with associated planning action.

Internal and External Audit

Internal audit plays a key role in reviewing controls, identifying system weaknesses and testing compliance with the ICB’s standing financial instructions.

External audit has a specific role to conduct an independent examination and express an opinion on the ICB’s financial statements.

The audit functions are separate and distinct from work to tackle crime, but it is important that there are effective links between those responsible for the audit function and those responsible for tackling economic crime.

Internal and external audit should meet regularly with those responsible for work to tackle economic crime, to discuss and monitor liaison requirements with reference to the purpose of each function, ensuring they remain effective and fit for purpose.

Any incident or suspicion of fraud, bribery, or corruption that comes to the attention of internal audit or external audit is to be passed immediately to the Counter Fraud Team.

People and OD function

Managers are responsible for taking forward disciplinary proceedings against employees who have committed an offence. People Directorate staff provide advice regarding this process in line with the ICB Disciplinary Policy. It is not unusual for criminal and disciplinary processes to overlap. In the case of parallel criminal and disciplinary processes, these should be conducted separately and by different officers, but there needs to be close liaison between those investigating economic crime and those progressing disciplinary proceedings since one process may impact on the other. This may include the sharing of information where lawful and at the appropriate time.

The People and OD function will, where appropriate, provide information to assist those responsible for dealing with economic crime with any proactive reviews undertaken in relation to detection or prevention activities. In addition, People Directorate will inform those responsible for investigating economic crime of any possible system weaknesses that could allow fraud, bribery, or corruption to occur. This includes weaknesses discovered as any part of a People Directorate investigation that did not warrant the commencement of a criminal investigation.

Those responsible for dealing with economic crime may need to meet regularly with members of staff from the People Directorate to discuss requirements to liaise and to monitor joint working arrangements.

Nominated and Accredited Local Counter Fraud Specialists (LCFS)

Nominated and accredited LCFSs work within NHS commissioning and provider organisations to tackle economic crime in line with the NHS CFA Counter Fraud Strategy.

The LCFS is responsible for anti-fraud work within the ICB and reports directly to the Executive Director of Finance & Commercial.

The LCFS reports to the Executive Director of Finance & Commercial, but any staff at the ICB can speak to and ask for advice from the LCFS. They are authorised to receive reports of suspected fraud from anyone, whether an employee of the ICB, independent contractor or other third party. All staff have a responsibility to the ICB to raise their genuine concerns.

The role of the LCFS is to ensure that all cases of actual fraud, bribery, and corruption are notified to the Executive Director of Finance & Commercial and reported accordingly. The LCFS will report to the Executive Director of Finance & Commercial on the progress of the investigation and if a referral to the police is required.

The investigation of most cases of alleged fraud within the ICB will be the responsibility of the LCFS. The NHS CFA will only investigate cases which should not be dealt with by the ICB, for example cross-boundary or national issues. Following receipt of all referrals, the NHS CFA will add any known information or intelligence and, based on their case acceptance criteria, will determine whether a case should be investigated by the NHS CFA.

The LCFS works with colleagues and stakeholders to promote anti-fraud work and effectively respond to system weaknesses and investigate allegations of fraud, bribery, and corruption. This will include the undertaking of risk assessments to identify fraud, bribery, and corruption risks at the ICB.

The LCFS employs a risk-based methodology to enable the ICB to target resources at high-risk areas and throughout the year undertakes proactive reviews in these areas that can detect fraud. Such reviews together with investigations enables the LCFS to identify and counter vulnerabilities within ICB systems by implementing effective prevention, detection, and corrective controls to reduce the likelihood of fraud.

Information Management and Technology

In line with the Computer Misuse Act 1990, the Digital and Business Intelligence Directorate will report all cases to the LCFS where there is suspicion that IT is being used for fraudulent purposes. This includes inappropriate Internet or E-mail use.

Policy Authors

The policy author will have responsibility for reviewing and updating the policy in line with Section 10 below.

Associate Director of Governance (Governance Lead) and Associate Director of Financial Management, Accounts and Financial Services

The Associate Director of Governance and Associate Director of Financial Management, Accounts and Financial Services will act as champions for counter fraud and liaise with the Local Counter Fraud Specialist (LCFS) to support agreed workplans and ensure the ICB meets its statutory duties.

Line Managers

All managers are responsible for ensuring that policies, procedures, and processes within their work areas are adhered to and kept under review. This includes but not limited to authorising annual leave, staff expenses and staff leave as appropriate following guidelines. Managers should ensure that an adequate level of internal control exists within their areas of responsibility and that controls operate effectively.

Managers should ensure that all employees in their teams are aware of fraud, bribery, and corruption (economic crime) risks and understand the importance of protecting the ICB against them. Managers may also be responsible for the enforcement of disciplinary action for employees who do not comply with policies and procedures and commit economic crime.

If a manager suspects, or is made aware, that someone in their team or a third party may be committing economic crime, they must immediately report their suspicions to the ICB LCFS and / or to the ICB’s Executive Director of Finance & Commercial or to the NHS CFA.

It is appreciated that some employees will initially raise concerns with their manager; however, managers should in no circumstances investigate suspicions or an allegation themselves. A summary of what employees (including managers) should do with any concerns is included in Appendices A and B. Routine verification of information or outliers according to normal processes is reasonable. However, where there is a concern that deliberate wrongdoing or potential fraud may have taken place, or they are unsure, employees (including managers) are encouraged to seek the advice of the relevant ICB LCFS at the earliest possible stage.

Managers must ensure all staff complete counter fraud training available on the Electronic Staff Record (ESR) as part of Essex ICB mandatory training requirements.

All Staff

All employees should carry out their duties with due regard for ICB policies and procedures, be aware of fraud, bribery, and corruption (economic crime) risks and understand the importance of protecting the organisation against them.

Employees must report any suspicions of economic crime as soon as they become aware of them, using the contact details listed in Appendix B, to ensure they are investigated appropriately and to maximise the chances of financial recovery.

Under no circumstances should any staff member commence an investigation into suspected or alleged economic crime. A summary of what staff should do with any concerns is included in Appendix B and Appendix C. Where there is a concern of deliberate wrongdoing or potential fraud, or they are unsure, staff are encouraged to seek the advice of the Local Counter Fraud Specialist at the earliest possible stage.

All staff should cooperate with the Local Counter Fraud Specialists, as well as NHS CFA and other bodies, to facilitate work to tackle economic crime involving the NHS by:

- Providing information and intelligence

- Facilitating investigations; complying with NHSCFA strategy and guidance

- Not revealing information about open investigations to unauthorised persons (including journalists)

- Taking all appropriate steps to prevent, detect and investigate economic crime including:

- Appointing qualified/professional personnel to operate in accordance with relevant legislation and relevant standards and

- Ensuring that appropriate measures are included in all financial governance and system controls to tackle economic crime.

All employees should not be afraid to report genuine suspicions of fraud, bribery, or corruption. The Public Interest Disclosure Act 1998 protects those who have reasonable concerns and will not suffer discrimination or victimisation for following the correct procedures.

Any fraud, bribery, or corruption concerns received through the Raising Concerns Policy should be referred to the Counter Fraud Team as soon as possible and whistleblowers encouraged to report any future fraudulent concerns directly to the Local Counter Fraud Specialist in the first instance.

Employees should not confirm or deny the existence of an ongoing fraud investigation to any unauthorised individual (including journalists) without seeking prior approval from the LCFS or relevant NHS CFA investigator, as appropriate.

For details regarding responsibilities regarding the declaration of gifts and hospitality, refer to the Standards of Business Conduct, including Conflicts of Interest, Gifts and Hospitality and Commercial Sponsorship Policy for the organisation. For expectations regarding the Values, Aims, Principles, Behaviours and Accountability, refer to the Corporate Governance Handbook.

The Response Plan

Fraud, Bribery and Corruption

The ICB has conducted risk assessments in line with Ministry of Justice guidance to assess how bribery and corruption may affect the ICB, as well as Home Office and NHS CFA guidance on how to ensure fraud prevention procedures are robust. As a result, proportionate procedures have been put in place to mitigate identified risks.

The ICB has implemented key policies, which all staff are required to adhere to and should be read in conjunction with this section:

- Standards of Business Conduct, including Conflicts of Interest, Gifts and Hospitality and Commercial Sponsorship Policy (Ref C002)

- Freedom to Speak Up (Whistleblowing) Policy (Ref HR001)

- Forensic Readiness Policy (Ref C013)

Reporting Fraud, Bribery, or Corruption

The ICB will be robust in dealing with any fraud, bribery, or corruption issues, and can be expected to deal with any person who attempts to defraud the ICB, or engages in corrupt practices, in a timely manner.

The LCFS will conduct all investigations in accordance with all relevant guidance and legislation. In particular, in full compliance with the NHS Counter Fraud and Corruption Manual issued by the NHS CFA.

Upon receipt of a referral, the LCFS must comply with national regulations including the Government Functional Standard 013: Counter Fraud (Functional Standard).

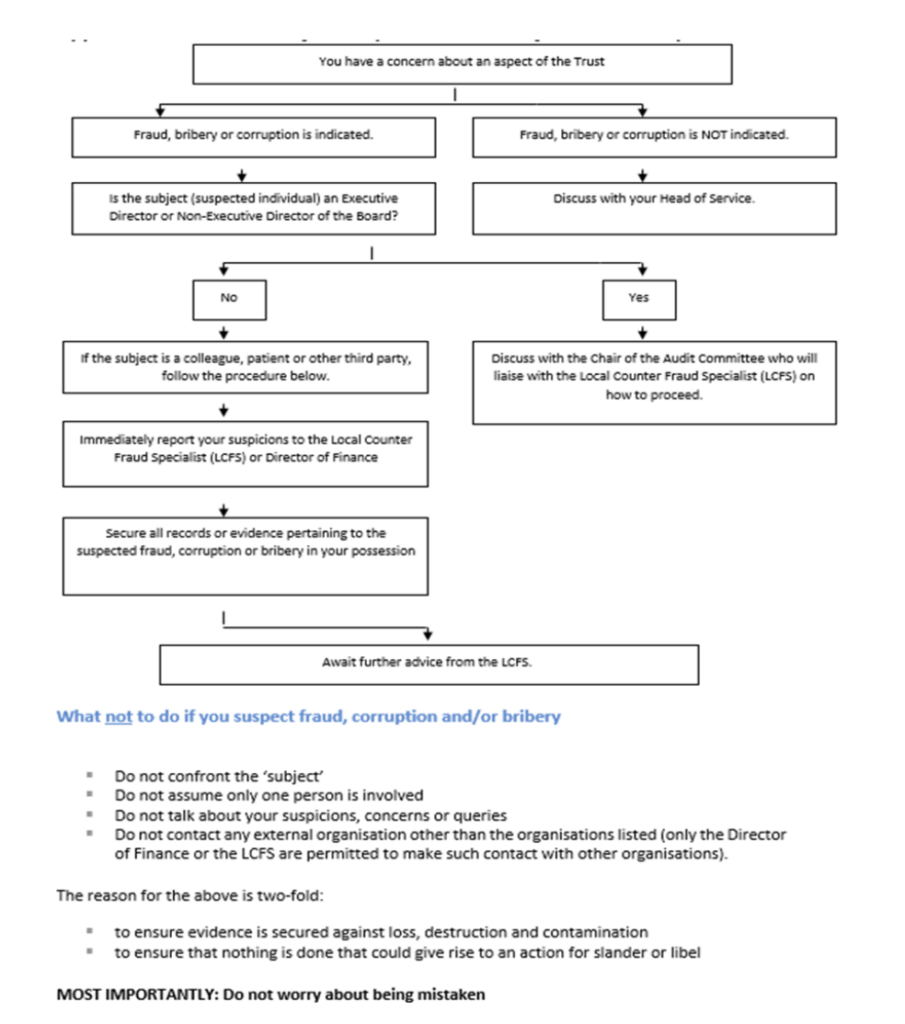

If there is good reason to suspect a colleague or other individual(s) of fraud, bribery, or corruption, the concerns should be reported to the LCFS or Executive Director of Finance & Commercial immediately. Suspicions of fraud, bribery or corruption may also be reported to the NHS CFA.

If there is a concern that the LCFS or Executive Director of Finance & Commercial themselves may be involved in suspected fraud, bribery, or corruption, the concerns can be reported to the ICB’s Chief Executive, Audit Risk and Compliance Committee Chair, or Chair of the Board.

Sufficient enquiries will be made by the LCFS to establish whether there is any foundation to the allegations. If the allegations are found to be malicious, they will also be considered for further investigation as to their source.

Suspicions of fraud, bribery, or corruption should be reported using the reporting lines detailed within Appendix B of this policy.

Responding to an Allegation

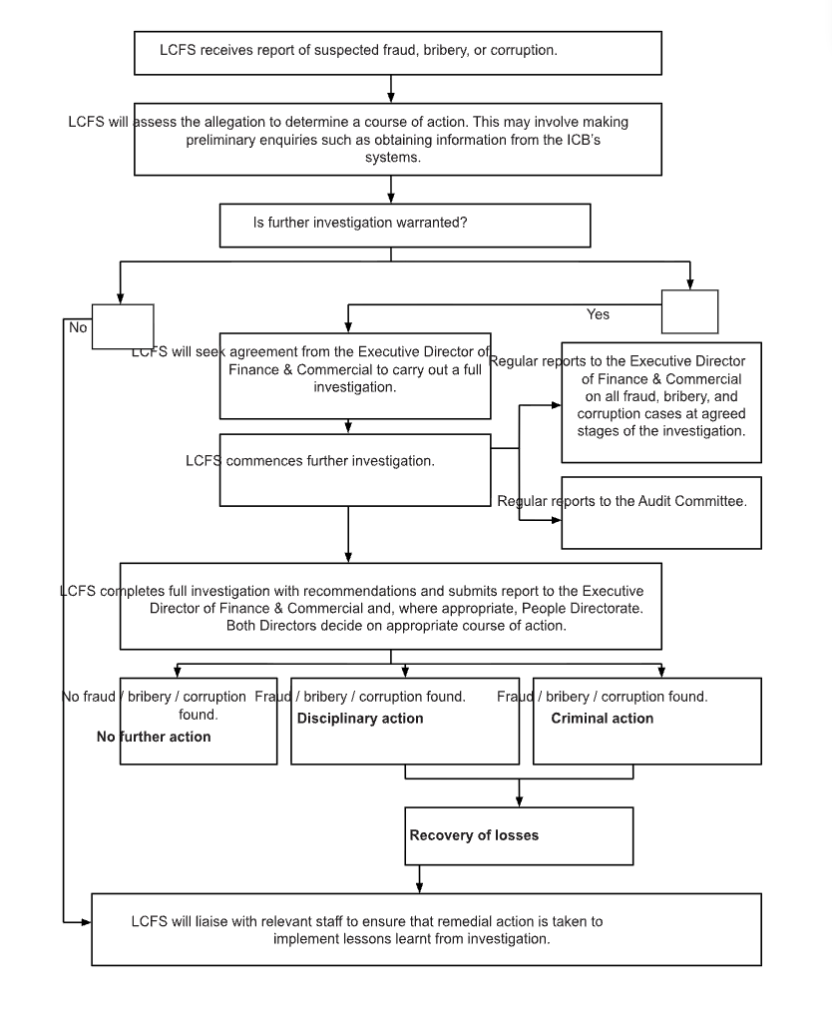

The LCFS is responsible for investigating all instances of fraud, bribery, or corruption at the ICB.

Upon receipt of a referral / allegation of fraud, the LCFS will assess the allegation to determine a course of action. This may involve making preliminary enquiries, such as obtaining information from ICB systems. After such preliminary enquiries, where appropriate, the LCFS will seek agreement from the Executive Director of Finance & Commercial to undertake an investigation.

If a criminal event is believed to have occurred but fraud, bribery, or corruption is not suspected, the police must be informed and the Local Security Management Specialist (LSMS) contacted if theft or arson is involved and, where appropriate, the Board and external auditors, in accordance with the ICB’s Standing Financial Instructions.

The LCFS will report regularly to the Executive Director of Finance & Commercial on all fraud, bribery, and corruption cases they investigate, as particular stages, of individual investigations. In addition, the LCFS will provide updates to the Audit Committee with updates at meetings as to the progress of investigations.

Detailed arrangements for the investigation of any suspected fraud, bribery, or corruption are contained within the NHS Counter Fraud and Corruption Manual and within relevant ICB policies. The LCFS will record the progress of each investigation in accordance with the legal codes of practice (Police and Criminal Evidence Act 1984, Regulation of Investigatory Powers Act 2000, Criminal Procedures and Investigation Act 1996, and other legislative requirements e.g., Data Protection Act 2018.

Upon conclusion of an investigation, the LCFS will report their findings and any recommendations to the Executive Director of Finance & Commercial. The Executive Director of Finance & Commercial is the sole person who can determine whether formal action is justified and what form such action takes; however, guidance can be sought, where required.

If the Executive Director of Finance & Commercial decides that formal action is to be taken against the subject(s) of an investigation, the LCFS will comply with the NHS CFA’s ‘Applying Appropriate Sanctions Consistently’ policy. This will involve using a sanction, or combination of sanctions, as follows:

- Disciplinary action: internal and / or professional regulatory body (warning, dismissal).

- Civil action: recovery of money, interest, and costs.

- Criminal prosecution: may result in imprisonment, community penalty, fine, confiscation, or compensation.

The use of parallel sanctions or the ‘triple track’ approach helps to maximise the recovery of NHS funds and assets whilst minimising duplication of work.

The ICB’s Disciplinary Policy will be used where the outcome of the investigation indicates improper behaviour on the part of staff. The LCFS shall liaise with the People Directorate regarding the provision of evidence for disciplinary hearings. Where the ICB has suffered a financial loss from a fraud, the ICB will pursue recovery in all applicable cases, subject to authorisation from the Executive Director of Finance & Commercial.

Sanctions and Redress

The types of sanction which the ICB may apply when a fraud, bribery, or corruption offence has occurred are as follows:

- Civil – Civil sanctions can be taken against those who commit fraud, bribery, and corruption to recover money and / or assets which have been fraudulently obtained, including interests and costs.

- Criminal – The LCFS will work in partnership with the NHS CFA, the police, and / or the Crown Prosecution Service (CPS) to bring a case to court against the offender. Criminal prosecution can potentially result in fines, imprisonment, community penalties, confiscations, and / or compensations, as well as a criminal record.

- Disciplinary Action by the Employing Body – Disciplinary procedures will be pursued by the ICB where an employee is suspected of being involved in a fraudulent or illegal act or when their negligent action has led to a fraud being perpetrated. Further information can be found in the ICB Disciplinary Policy. It should be noted, however, that the duty to follow disciplinary procedures will not override the need for legal action e.g., consideration of criminal action. In the event of doubt, legal statute will prevail.

- Disciplinary Action by a Regulatory Body – If warranted, an employee may be reported to their professional body as a result of an investigation and / or prosecution.

- Financial Recovery – The ICB will seek financial redress whenever possible to recover losses to fraud, bribery, or corruption. Redress can take the form of confiscation under the Proceeds of Crime Act 2002, compensation orders, a civil order for repayment, or a local agreement between the ICB and the offender to repay monies lost. Financial redress resources that are lost to fraud, bribery, or corruption to be returned to the NHS for use as intended.

Approach to Tackling Economic Crime

Strategic Governance

The ICB will ensure there is support for work to tackle Economic Crime at all levels with the organisation. The Executive Director of Finance & Commercial will have overall responsibility for overseeing and providing strategic management and support for the work, ensuring it is embedded across the ICB. All counter fraud work will be aligned to the NHS CFA strategy.

Furthermore, the ICB will undertake the full range of work against economic crime.

A local risk assessment based on the NHS CFA Risk Descriptors and other influencing factors will form the basis of an annual Counter Fraud Plan setting out the work scheduled for the year and authorised by the Audit Committee.

Key Principles for Action

In order to tackle economic crime, the ICB will take a multi-faceted approach that is both proactive and reactive. This approach is set out in the following three key principles for action:

Inform and Involve

The ICB will ensure all its employees understand what economic crime is, and their role in ensuring they follow the correct reporting procedures. This can take place through communications and promotions, such as awareness campaigns, newsletters and presentations.

Prevent and Deter

The ICB will remove opportunities for economic crime to occur and discourage those individuals who may be tempted to commit these crimes. Successes will be publicised so that the risk and consequences of detection are clear to potential offenders. Those individuals who are not deterred should be prevented from committing crime by ensuring robust systems are in place.

Hold to account

The ICB will ensure those who have committed economic crime against it are held to account for their actions. Essex ICB will ensure professionally trained specialists are in place to detect and investigate these offences and will seek to apply the full range of sanctions to those found to have committed fraud, bribery or corruption, including criminal, civil and disciplinary sanctions. Disciplinary sanctions will be carried out by People Directorate supported by the LCFS as appropriate.

The ICB will also seek to recover all funds lost to economic crime.

Monitoring Compliance

Awareness of and compliance with the policies and procedures laid down in this document will be monitored by NHS CFA, as part of their quality assurance programme. Independent reviews may be conducted by both Internal and External Audit on a periodic basis.

Service Conditions Section 24 of the Standard NHS Contract relates to the expectations surrounding anti-crime arrangements. Under the NHS Standard Contract, all organisations providing NHS services are required to put in place appropriate counter fraud arrangements.

The Government Functional Standard 013: Counter Fraud sets the expectations for the management of fraud, bribery, and corruption risk in government organisations and wider public services, whilst reinforcing the government’s commitment to fighting fraud against the public sector. Since April 2021, all NHS organisations have been required to provide assurance against the Functional Standard. This should be overseen by the ICB’s Executive Director of Finance & Commercial, as the accountable officer for fraud, and Audit Risk and Compliance Committee and in line with the ICB’s existing approach against counter fraud requirements.

On an annual basis, organisations are expected to complete a year-end return against the Functional Standard, and to submit the results to the NHS CFA. The LCFS submits the year-end return against the Functional Standard, after signed agreement and approval from the Executive Director of Finance & Commercial and Audit Risak and Compliance Committee Chair.

The LCFS will produce an annual report, providing a summary of the work conducted against components of the Government Functional Standard. To comply with the Functional Standard, the annual report must also include a copy of the year-end return and a statement signed by the Executive Director of Finance & Commercial. The annual report is presented to the Audit Risk and Compliance Committee for approval.

Implementation and Staff Training

Managers must ensure all staff complete the counter fraud training as part of the ICB’s training requirements.

Raising awareness of fraud, bribery, and corruption amongst staff is a key part of creating a strong anti-fraud, bribery, and corruption culture where fraudulent and corrupt activity is not tolerated and all staff and contractors are aware of their responsibility to protect NHS funds, as well as the correct reporting procedures. A strong anti-fraud, bribery, and corruption culture provides the organisation with assurance the fraud is recognised and reported.

Arrangements for Review

This policy will be reviewed no less frequently than every two years. An earlier review will be carried out in the event of any relevant changes in legislation, national or local policy/guidance, organisational change or other circumstances which mean the policy needs to be reviewed.

Views and input from the ICB’s Local Counter Fraud Specialist will be sought as part of the policy review process.

If only minor changes are required, the sponsoring Committee has authority to make these changes without referral to the Integrated Care Board. If more significant or substantial changes are required, the policy will be ratified by the relevant committee before final approval by the Integrated Care Board.

Associated Policies, Guidance and Documents

- Freedom to Speak Up: (Whistleblowing) Policy (Ref HR001)

- Standards of Business Conduct, including Conflicts of Interest, Gifts and Hospitality and Commercial Sponsorship Policy (Ref C002)

- Disciplinary Policy (Ref HR015)

- Forensic Readiness Policy (Ref C013)

References

- NHS Counter Fraud Strategy

- Fraud Act 2006

- Bribery Act 2010

- NHS CFA Anti-Fraud Manual

- NHS CFA Applying Sanctions Consistently

- Government Functional Standard 013: Counter Fraud (Functional Standard)

- Public Interest Disclosure Act 1998

- Criminal Procedure and Investigations Act 1996 (the CPIA Code)

- Computer Misuse Act 1990

- Criminal Justice Act 2003

- Proceeds of Crime Act (POCA) 2002

- Police and Criminal Evidence (PACE) Act 1984

- Data Protection Act (DPA) 2018

- General Data Protection Regulations (GDPR)

- Economic Crime and Corporate Transparency Act 2023 (ECCTA)

Equality Impact Assessment (EIA)

The EIA has identified no equality issues with this policy.

The EIA has been included as Appendix A.

Appendix A – Equality Impact Assessment

Initial information

Name of policy and version number: Counter Fraud, Bribery and Corruption Policy v1.0

Directorate/Service: Corporate Services

Assessor’s Name and Job Title: Jane King, Corporate Services & Governance Support Manager

Date: March 2026

Outcomes

Evidence

Analysis of impact on equality

The Public Sector Equality Duty requires us to eliminate discrimination, advance equality of opportunity and foster good relations with protected groups. Consider how this policy / service will achieve these aims.

N.B. In some cases it is legal to treat people differently (objective justification).

- Positive outcome – the policy/service eliminates discrimination, advances equality of opportunity and fosters good relations with protected groups

- Negative outcome – protected group(s) could be disadvantaged or discriminated against

- Neutral outcome – there is no effect currently on protected groups

Please tick to show if outcome is likely to be positive, negative or neutral. Consider direct and indirect discrimination, harassment and victimisation.

| Protected group | Positiveoutcome | Negative outcome | Neutraloutcome | Reason(s) for outcome |

|---|---|---|---|---|

| Age | ✔ | No impact identified. | ||

| Disability(Physical and Mental/Learning) | ✔ | No impact identified. The policy will be made available in alternative formats, such as easy read or large print and alternative languages upon request. The policy has also undergone website accessibility checks. | ||

| Religion or belief | ✔ | No impact identified. | ||

| Sex (Gender) | ✔ | No impact identified. | ||

| Sexual Orientation | ✔ | No impact identified. | ||

| Transgender / Gender Reassignment | ✔ | No impact identified. | ||

| Race and ethnicity | ✔ | No impact identified. The policy will be made available in alternative formats, such as easy read or large print and alternative languages upon request. | ||

| Pregnancy and maternity (including breastfeeding mothers) | ✔ | No impact identified. | ||

| Marriage or Civil Partnership | ✔ | No impact identified |

Monitoring outcomes

Monitoring is an ongoing process to check outcomes. It is different from a formal review which takes place at pre-agreed intervals.

Review

Appendix B – What to do if you have any suspicions of fraud?

Appendix C – How to report suspected fraud taking place in the NHS

All calls are dealt with in the strictest confidence and callers may remain anonymous.

Suspicions of fraud, bribery, or corruption should be reported to any of the following:

Contact details

Local Counter Fraud Specialist

- Hannah Wenlock, LCFS:

- 0845 300 3333

- Hannah Wenlock, LCFS:

- 07919 595930

- Email:

- [email protected]

- Email:

- [email protected]

Contact details

Executive Director of Finance & Commercial

- Jennifer Kearton:

- 07768142801

- Email:

- [email protected]

Contact details

ICB’s Audit Chair (TBD)

Contact details

National Fraud and Corruption Reporting Line

- Phone number:

- 0800 028 4060

Contact details

Public Concern at Work. This is an independent charity who can offer advice on how to proceed

- Public Concern at Work:

- 020 7404 6609.

Report fraud online at: https://cfa.nhs.uk/reportfraud

Important notice

All referrals will be treated in complete confidence. Staff can raise concerns anonymously if they prefer to do so.

The ICB has a Freedom to Speak Up: Raising Concerns (Whistleblowing) Policy. The policy enables you to raise your concerns at an early stage and in the right way. The policy can be accessed via Freedom to Speak Up (Whistleblowing) Policy (Ref HR001).

Appendix D – Fraud, Bribery, and Corruption Response Plan